The Good, the Bad and the Unclear : Environmental Budget Tagging

This study takes stock on the experience of some twenty countries and several international development institutions in Environmental Budget Tagging. It identifies the expected benefits and the conditions to achieve them: take into account the measures that are unfavorable to the environment, consider the outcomes of assessed measures and not only their intention, repeat the exercise over time and fit it into the existing administrative culture and processes…

Climate and environmental issues affect all aspects of a nation’s economic life. Acknowledging this reality, more and more finance ministries are implementing tools to facilitate and optimize the consideration of the environment in budgetary decisions, known as “green budgeting” tools. The Environmental Budget Tagging (EBT) is one such tool, which aims to highlight all budgetary measures related to one or more dimensions of environmental action, such as climate change, biodiversity or land degradation.

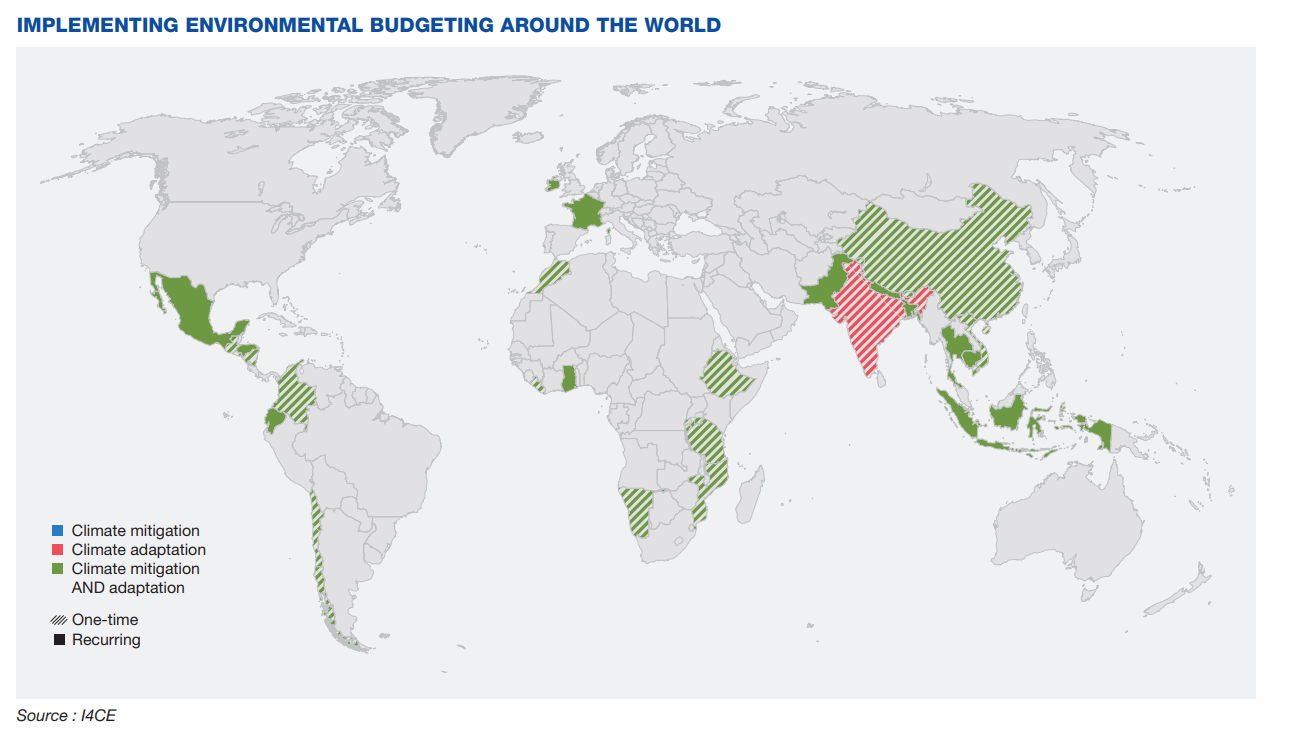

This review tries and provides answers to two questions: What are the expected benefits of these tools? Under what conditions are they achieved? It takes stock on the experience of some twenty countries and several international development institutions (UNDP, IDB, World Bank, OECD), through bibliographic reviews and a large series of interviews with national practitioners, researchers, and experts from various international institutions. 10 case studies (8 from Latin America + Indonesia and France) were examined in depth, their conclusions and comparisons being compiled in a methodological annex to this report. In particular, the study focuses on the differences between “minimal” and comprehensive evaluations, finding that the significant additional benefits associated with a comprehensive evaluation more than justify the additional effort involved.

Some design choices for an EBT must be made well in advance, as they strongly structure the entire evaluation.

Such choices fall into two categories:

• methodological criteria : to be effective, a EBT must encompass a broad scope of budgetary measures, evaluate expenditures but also taxes, take into account the expected outcomes of assessed measures and not only their intention, identify measures that are unfavorable to the environment… The analysis should thus go beyond considering the environmental effort, and aim to evaluate the coherence of the budget with national objectives.

• process criteria : the full effects of a EBT are felt under two conditions:

– excellent national ownership : the EBT must first and foremost respond to a context-specific need, clearly identified upstream, with internal resources. It must also fit into the existing administrative culture and processes, in coherence with other national green budgeting tools.

This seems a simple requirement, but it often proves a stumbling block, as the perceived technical complexity and resource requirements of EBTs pushes ministries to rely on external expertise not only for designing, but also for carrying on, the work.

Click on this button to see the image

– a long-term perspective : an EBT should not be a one-time exercise, but an effort to be maintained over time. This is of course necessary in order to measure the improvement or deterioration of indicators and to correct the national trajectory in “real time”; but it is also important in order to give certain processes time to take hold. In particular, it is by maintaining the exercise over time that one will be able to go beyond quantitative considerations regarding monetary volumes alone and open the dEBTte on the environmental effectiveness of the overall policy mix; it is also over time that discussions, acculturation and capacity building of the various actors can arise – and it is through these fundamental changes that an EBT has the most impact.

Under the conditions listed above, an EBT is useful both for the analytical results it produces and for the process that leads to these results. First, by improving the transparency of public action in areas where public expectations are high. Second, by establishing an interministerial dialogue that allows finance ministries and technical ministries to take ownership, within their own scope of expertise and action, of a complex subject given its very cross-cutting nature. Finally, by informing budgetary decisions with simple tools on issues that are highly complex, aggregating potentially scattered information and highlighting the cobenefits or undesirable effects of measures or packages that do not all have a stated climate objective. Finally, they provide reporting tools for international finance, both private (Green Bonds) and public (development banks), even if one must be careful because the financial incentive may bias the evaluation. That being said, one should not expect too much from such evaluations: EBTs are an important and relevant tool for the budgetary policy of a government with environmental objectives, but it is only a tool, and a rather technical one at that. It is only useful if it serves strong political action, and as part of an ecosystem of green budgetary decision-making and planning tools.

{kind=link}