Financial Regulation and Climate : Next steps to follow in the coming months

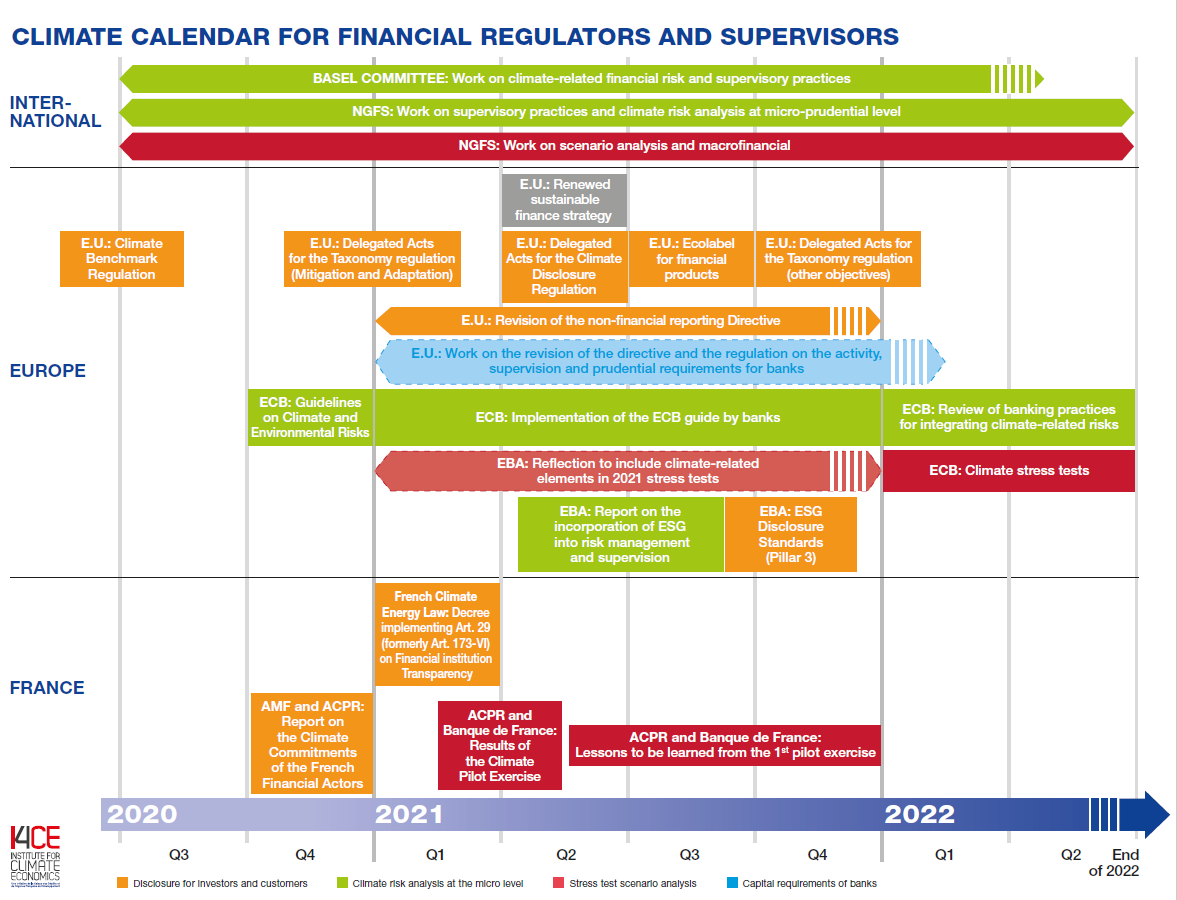

The public institutions that regulate and supervise private finance will talk a lot about climate change in the coming months. The European taxonomy that allows economic actors to identify activities that are favorable to ecological transition or the “climate stress tests” of the Banque de France and ACPR are just some of the issues that we invite you to follow. I4CE has synthesized for you the “climate calendar” of financial regulation in a graphics.

Network of Central Banks and Supervisors for the Greening of the Financial System (NGFS), European Central Bank (ECB), European Banking Authority (EBA), Banque de France, Autorité de contrôle prudentiel et de résolution (ACPR), Autorité des marchés financiers (AMF)… In recent years, new actors – financial regulators and supervisors – have emerged in public policy discussions against climate change. Think tanks, NGOs and academics have timidly begun to take an interest in the role of these institutions in the low-carbon transition, and these institutions have for their part gradually taken up the subject, mainly from the perspective of the risks that climate disruption could cause to finance stability.

There is now a political and technical agenda around financial regulation and climate, and there will be key moments in the coming months that we all need to keep in mind. Important agendas will come to the table of regulators and supervisors, whether in the form of revised directives, new decrees, progress monitoring reports or recommendations for best practices. Important issues for the experts and regulators themselves, but hopefully also more widely for parliamentarians, NGOs, the media…. In a context marked by numerous initiatives from the European Commission and financial supervisors, it is important to stimulate debate on the objectives of financial regulation and the means to achieve them.

How can we find our way through this proliferation of initiatives? Our graphics show the issues to be monitored over the next 18 months and the major challenges they address (climate transparency, climate risks, etc.). It specifies when these issues will be discussed and the institutions involved, and provides links to more information.

Click on this button to see the image

Access the clickable links of the graphic

ISSUE 1. Improving the climate transparency of players and financial markets

Having quality information on the actions taken by economic players – financial or otherwise – is necessary for several reasons. In the eyes of regulators, climate transparency contributes to the proper functioning of financial markets, but this information is just as necessary to monitor the commitments made by financial players and avoid greenwashing, or to help savers find their way around the multitude of “sustainable” financial offerings. To meet this challenge, regulatory changes are expected in France and Europe in 2021 on the non-financial transparency of financial players and more broadly of companies. The implementation of the European taxonomy will also be an issue to be monitored in the coming months: to be transparent about what is good – and bad – for the climate, a financial player needs to know what is good for the climate and more generally for environmental transition. From now on, he will be able to refer to this classification developed and adopted at the European level.

ISSUE 2. Encouraging financial actors to better integrate climate risks into their decisions and ISSUE 3. Encouraging financial actors to assess their global exposure to climate risks

Financial regulators and supervisors are sensitive to the risks, and therefore naturally to the risks that climate change and the low-carbon transition pose to financial players and financial stability. They want these risks – for example, the sudden depreciation of all investments and credits in fossil fuels – to be assessed and taken into account. The challenge of climate risks is twofold for regulators. They must ensure that financial players integrate climate risks into their investment or credit granting decisions. To this end, the NGFS and a special Task Force of the Basel Committee will continue their work on climate risk analysis and supervision practices in 2021. For example, they are considering the best practices for managing climate risks that they will recommend to financial players . Supervisors must also ensure that financial players understand and assess their overall exposure to climate risks, hence their work in 2021 on “climate stress tests” or scenario analysis. The NGFS will soon specify the types of reference scenario to be used. The European Banking Authority at the European level, the Banque de France and the ACPR in France will continue their discussions with stakeholders or publish the results of their pilot exercise in the coming months.

ISSUE 4. Adapting banks’ capital requirements to climate issues

In banking matters, regulators have powerful leverage: they define the amount of capital that banks must build up to cover unexpected losses in the event of a crisis. They could therefore decide that a bank that invests in a fossil fuel project must increase its level of capital against these liabilities. Or vice versa. While many players want to change capital requirements regulations to “climate proof” them, regulators are reluctant to do so. This is an important issue, a difficult debate that tends to mix different possible objectives. In any case, it is an issue to be followed in 2021: the European Commission will study the revision of its regulations and directive on capital requirements for banks.

{kind=link}